All venture capital funds hire highly skilled people to copy-paste data and maintain an updated dealflow database. If you recognize your company in the first sentence, have no worries, you are not the only one. Many investors do the same. But not the best performing investors.

When it comes to companies’ research, data collection and reporting, the amount of admin work is piling up. Therefore, in our continuous endeavor to bring you the most valuable solutions, we are sharing a common practice of the best performing investors – data entry automation.

We are introducing the PitchBook – Edda integration.

PitchBook is a financial data and software company. Pitchbook provides thousands of businesses and investors with comprehensive data on private markets. One of their main aims is to help investors discover and execute opportunities with confidence and in a time-efficient manner.

Edda customers will now have access to more private market data than anyone else. For instance, they will be able to choose Pitchbook, amongst our other integrated sources and databases, to quickly pull information on any potentially interesting company. And the best thing about it- the process is very simple and it takes only a few seconds and clicks.

How Does PitchBook – Edda Integration Work?

As said, the process for leveraging the access to PitchBook from Edda’s dealflow venture capital management software is effortless and time-efficient:

Login to the deal-flow platform and start adding the new companies to you pipeline.

As you start typing the company name the system is automatically going to offer you the choice of data sources. Pick the preferred one to pull the company data from.

Click on your preferred data source and the company will be added to your pipeline. At the same time all available data from the source will be populated in the company card.

Below, you can take a look at the entire process:

Finally, if you would like to find out more, schedule a demo and see how Kushim can help you out in finding your next investment unicorn.

Moreover, Pitchbook offers 10 free credits for all investors that request a demo and a trial of Edda’s venture capital software on our website.

In this article we will discuss the often posed question of “How to become a VC“. And let’s be honest from the start, becoming a VC is not an easy task.

First of all, there is no “official education“ for future Venture Capitalists. Even the experiences of today’s VC investors, founders and partners tell us that sometimes “climbing through the window” is the only way into the VC world. For instance, the case of Jan Garfinke who had over 20 years of experience in successful med-startups, taught us that founding your own VC firm may be an easier task than landing a high-position job within an existing one.

As a matter of fact, most VC professionals would agree that there is no straight path into the VC business. However, we could set up some general prerequisites or steps, if you are thinking of pursuing the VC career.

How To Become a VC: The Potential Steps

Knowledge of VC Operations

The in-depth knowledge of the VCs main processes, activities, goals, structures, problems etc. is crucial. Simply, knowing the VC business would definitely help you in gaining and shaping experiences matching their activities and processes. And having such development path prior to your first attempt of entering the VC industry could actually land you the first VC job.

Business School

Background

Naturally, having a top university and business school background (i.e. Ivy League), majoring in Economics, Finance, Business Management etc, is always a good start. It will equip you with both general knowledge and more specific business set of skills through highly reputed internships. And if those internships are done in VC firms, you know you are definitely on the right track.

The Startup Apprenticeship

A well shaped experience in startups is extremely important. Being a part of a successful startup or two will bring you in close connection with your investors- VC funds. Hence, through this close-cooperation you would not only gain invaluable insight into the VC operations in terms of deal sourcing and investing (your startup is going through this exact process), but you will also build relationships which could help you enter the next VC firm.

There are two levels at which we can see the startup step as beneficial and invaluable. On the one side, the aspiring VCs who shape their experience by being a part of several industry-diverse, successful startups will acquire knowledge and develop expertise in various fields. As a result, these VCs often turn out to be great investors since they have a wide range of industry expertise and are very analytical.

On the other side, if you are the founder of a successful startup, you will have the advantage of strong established networks (former employees and investors). In addition, you will be able to easily bond and “groom” the young entrepreneurs as you already walked their path. And finally, you will be considered an “expert“ in your industry field and therefore seen as a valuable addition to the VC team.

To conclude, both options have their strong points and there is no right or wrong choice here. However, one thing is certain, the step in a startup direction will definitely lead you a step closer to entering a VC firm.

Gain Experience In Consultancy Firms

Having experience in business consultancy firms as business developers, financial analysts or similar could also come in handy. For instance, here you would definitely gain experience in regards to assessing the business plans from various perspectives. This could prove very useful when aspiring to land a job as analyst/associate or even principal in a VC firm.

Alternative way to become a VC: Raise Your Own Fund

As we elaborated above, there are various steps you could take in order to enter the VC business. And depending on your development path, you could land an entry or higher level position job. However, this is not a given.

Even if you go through all of the hard steps, polish your CV and look like an ideal candidate for a VC position, you still may not get it. Sometimes, the only way to become a part of this world is to raise/start your own fund. And here, a whole new level of challenges await you.

First of all, without a proven record, gaining trust of LPs in raising your fund is going to be difficult. You have to think long and hard on the approach, the investment thesis and how you will “package and sell” your VC product, as VC fund is a product after all. Furthermore, you will have to prepare for substantial investment yourself, and have much more “skin in the game” in terms of the % of the total capital invested. Finally, with all the enthusiasm and knowledge you may possess, you will need to arm yourself with plenty of patience. Simply, finding and recognizing the unicorn in the startup environment is close to finding a needle in a haystack…

What is the right path to become a VC?

The answer is simple, there isn’t one. There is no right, set and paved road to entering the VC world, but rather a wide variety of approaches you could consider.

Although we cannot help you further with schooling and startup/consultancy firms’ experience, we can definitely help with the first step. A place where you can get a great insight into the VC business operations, requirements, and necessary software venture capital tools, whether you want to land a job or start your own fund is our e-book: VC Journey Explained. And it can definitely shed some light on how to become a VC.

Welcome back to Edda’s deep dive of fund performance analysis. In previous articles, we have discussed fundamental fund performance metrics such as IRR, TVPI, DPI and RVPI ratios. This article, however, will explore public market equivalents including the direct alpha method of assessing a fund’s performance.

The Foundation of Public Market Equivalent (PME)

Imagine you were investing in a particular stock market index such as S&P 500 for a period of ten years. Whenever you sell, you get a return. And now imagine that whenever a VC fund makes a capital call, it is exactly like investing in a stock market index and when the VC fund makes a distribution to its partners it is similar to selling the stock market index shares.

This is exactly the concept of PME. There are many different forms of PME such as Long Nickels PME, Kaplan and Schoar PME (KS PME), PME+ developed by Capital Dynamics, and mPME developed by Cambridge Associates. In addition, we will discuss the Direct Alpha method.

First, we must understand the foundation of PME.

The basic premise of PME is to calculate the future value of each cash flow as if they were invested in a stock market index. The formula to calculate future value is given below:

Let’s illustrate this with an example:

Assume on Dec 31, 2007 a VC fund made a capital call of $100 million and currently the date is Dec 31, 2017. The value of S&P 500 on Dec 31, 2007 was 1411.63 and the value of S&P 500 on Dec 31,2017 was 2743.15. Therefore, the future value of this cash flow is:

Long Nickels Index Comparison Method (ICM/PME)

The Long Nickels index comparison method was proposed by Austin M. Long III and Craig J. Nickels in 1996. It is considered to be the oldest and first PME method of assessing the performance of a VC fund. The basic idea of Long Nickels method is that the cash flows of a VC fund i.e. contributions and distributions are invested in a stock market index and to generate a net asset value (NAV) at the end of each period. The last NAV is used to calculate the IRR and this IRR is the Long Nickels PME.

For comparison, two IRRs are calculated, one is the fund IRR and the other is Long Nickels IRR. If the fund IRR is greater than Long Nickels IRR then the fund provided excess returns compared to the stock index and vice versa. Let’s illustrate Long Nickels PME with an example.

The data below shows the contributions and distributions of a VC fund along with the S&P 500 index value. The “index value change” column shows the percentage increase or decrease in the S&P 500 value

Net Asset Value (NAV)

At this point, we will calculate the Net Asset Value (NAV) at the end of each period. Here we will regard the contributions as positive cash flow and distributions as negative cash flow. The logic behind this assumption is that contributions are considered the amount that is invested in the hypothetical stock market index and this determines the net asset value. On the other hand, distributions is the amount paid back during the sale of stock index fund which decreases the NAV. For the purpose of calculation, only the last NAV will be taken into the final calculation of LN PME.

Lastly, we will calculate the net cash flow and find the IRR of Net cash flows. The NAV for the last period i.e. Jan 1, 2014 will be the NAV (ICM) we calculated above is 30.

Here, the fund IRR is 15% and the Long Nickels IRR is 12%. Hence the fund gave 3% excess returns compared to S&P 500 index.

Limitations of Long Nickels PME

The biggest drawback of LN PME is that a strong out-performance or under-performance can affect the IRR and it can produce a null value. For instance, this can be seen in the below table where a strong out-performance has reduced the ICM IRR to zero.

PME+ Value In Fund Performance Estimation

In the 2003 paper, ‘Private equity benchmarking with PME+’, Christoph Rouvinez introduced a new way of benchmarking the performance of a PE fund by using a coefficient lambda (λ) or a scaling factor to discount the value of distributions so that the NAV of the index matches the NAV of the fund. The PME+ returns an IRR value of discounted distributions. After that the discounted distributions are used to calculate Net Cash Flow and PME+ IRR calculated. If the PME+ IRR is less than that of the fund’s IRR then the fund has outperformed the stock index and vice versa.

The formula used to calculate new distribution is: Distribution x λ

Let’s illustrate PME+ with an example. First, we will calculate λ, which is found by using trial and error. The NAV of PME+ calculations must be equal to the fund’s NAV. In our example the PME+ NAV must be equal to 70.

The calculations to determine lambda and the subsequent steps make PME+ more complicated compared to LN PME method. For our data set, the lambda is found to be 0.9273. Now we will use the value of lambda to calculate the adjusted value of distributions.

The PME+ IRR is 12% while the fund IRR is 15%. Hence the fund has outperformed the stock market index.

Limitations of PME+

One of the challenges with computing PME+ is that the calculations are not simple. Secondly the usage of a single scaling factor λ is also sensitive to strong outperformance or underperformance. PME+ suffers from the common limitations associated with IRR calculations.

Kaplan Schoar (KS PME)

Nine years after the Long Nickels PME was introduced, Steven N. Kaplan and Antoinette Schoar introduced the KS PME method in 2005. The objective of KS PME method was to address the shortcomings of Long Nickels PME. Instead of choosing an IRR measure, the KS PME represents a market adjusted equivalent of the Total Value to Paid-In-Capital (TVPI). KS PME is calculated by finding the future value of each contribution and distribution using the stock market index returns. The formula for KS PME is given below.

A KS PME multiplier equal to 1.0 means that the VC fund has delivered a performance equal to the stock market index. Therefore, a KS PME multiplier of more than 1.0 means that the VC fund performed better than the stock market index and a multiplier of less than 1.0 means that the VC fund provided returns lower than that of the stock market index. Currently, the KS PME is considered most superior and widely used PME.

Example: Let’s illustrate the KS PME method with an example. The future values will be calculated using the future value formula discussed at the beginning of this post.

The KS PME multiplier of 1.068 suggests that the VC fund performed marginally better than the public index. Higher the KS PME multiplier, higher or more substantial is the fund performance as compared to a stock market index.

Limitations of KS PME

The KS PME removes the IRR sensitivity problem of Long Nickels PME. However, it ignores the timing of cash flows.

Modified PME (mPME)

The modified PME or mPME was introduced by Cambridge associates in 2013. mPME is similar to PME+ in the sense that it uses a scaling factor. However, mPME uses different scaling factors for cash flows at different time intervals. Thus, it attempts to improve the limitations of PME+ where a single coefficient λ is used to scale all distributions. The steps to calculate mPME are the following:

1. Calculate the Distribution weight for each distribution using the formula:

2. Calculate a hypothetical NAV called NAVPME using the formula:

3. Calculate the weighted distribution using the formula:

4. Finally, the net cash flow is calculated using the adjusted distribution and the IRR of this net cash flow gives us the mPME IRR.

Let’s simplify the complicated mPME calculation with an example: The NAV in light grey shade is market determined NAV. First, we will determine the Dweight

After that, we will find the NAVPME, the column It/I(t-1) refers to index values, this will simplify the calculations:

Now we will calculate the adjusted value of distribution:

Finally, we will use the adjusted distribution to calculate the net cash flow and compute the mPME IRR.:

The mPME IRR is 13.91% whereas the fund’s IRR is 15%. Hence mPME IRR indicates that the fund performed marginally better than the stock market index.

Limitations of mPME

The mPME measure seeks to improve the Long Nickels PME just like the PME+ method. However, it again uses a scaling factor to adjust the distributions, hence it is prone to manipulation and sensitive to under or outperformance. It also doesn’t take the future value into account and as evident from our calculations, mPME is much difficult to compute.

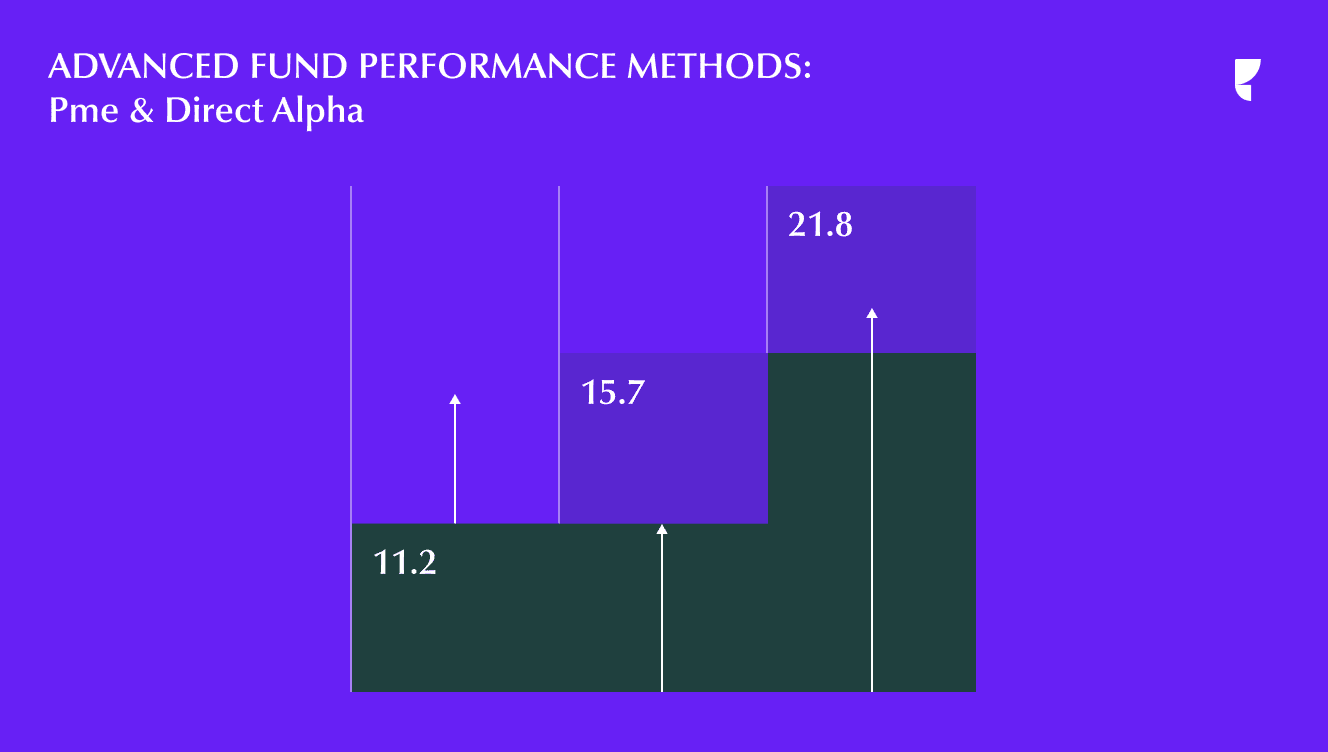

Direct Alpha As A Fund Performance Method

The direct alpha method is the most recent one and it was introduced in 2014 by Oleg Gredil, Barry E Griffiths and Rudiger Strucke. In 2009, Grifiths had talked about the concept of alpha which basically refers to the excess return a VC/PE fund makes as compared to a public market index and also points to fund managers superior performance.

The concept of direct alpha is closely related to the KS PME as it uses the same method to calculate an IRR which is then compared to the fund’s IRR. However, the difference between KS PME and direct alpha method is that in direct alpha the under or out performance is quantified by calculating the compounded cash flows plus the fund’s NAV.

Let’s illustrate direct alpha with an example. The future value of both contributions and distributions is found by using the future value formula discussed at the beginning of this post.

The Direct Alpha IRR is calculated to be 3% while the fund IRR is 15%. Since the direct alpha IRR is lesser than that of the fund IRR, this means that the fund outperformed the market index. In conclusion, of all the PME methods, direct alpha is the only method that tries to overcome the limitations and provide an exact number of outperformances rather than giving an approximate value of outperformance.

References

Long, A.M. III & Nickels, C.J. (1996). A Private Investment Benchmark. The University of Texas System, AIMR Conference on Venture Capital Investing.

Rouvinez, C. (2003). Private equity benchmarking with PME+. Private Equity International, August, 34–38.

Kaplan, S. & Schoar, A. (2005). Private Equity Performance: Returns, Persistence, and Capital Flows. Journal of Finance, 60, 1791–1823.

Griffiths, B. (2009). Estimating Alpha in Private Equity, in Oliver Gottschalg (ed.), Private Equity Mathematics. 2009, PEI Media.

Cambridge Associates (2013). New Method for Comparing Performance of Private Investments with Public Investments Introduced by Cambridge Associates.

Gredil, Oleg and Griffiths, Barry E and Stucke, Rüdiger, (2014). Benchmarking Private Equity: The Direct Alpha Method.

Capital Dynamics. (2015). Public benchmarking of private equity Quantifying the shortness issue of PME.

This week we spoke with Nicolas Rabrenović – the CTO & Co-founder of Edda about the challenges of working at a fintech startup in the development phase.

Can you introduce yourself ?

Hi, I’m Nicolas, Co-founder and CTO @Edda.

What’s your background ?

I’m passionate about science, technology and finance. When I was a kid, I was a geek who participated in chess tournaments, made websites for pocket money and learned about the stock market. I have never been passionate about school but somehow I graduated with a double Masters in technology for Web School Factory and HETIC in Paris.

During my studies in Paris, I met Clément Aglietta, Alexandre Crenn, Victor Espinet and Josselin Lebail. And this is where the story of Edda’s venture capital software began.

Describe a day in your life:

On some days, I am in Paris with the management team and on other days, I am in Belgrade with the tech team.

When you work in a tech startup, you get exposed to new topics everyday and that keeps your day more dynamic.

My typical day consists of making sure that the company can grow safely, the work flow with the team is smooth and that everyone is aware of the next steps.

I have a final word with the team about the technologies we will use in order to help the strategy side on every topic related to tech.

Additionally, I talk to our customers if they have any questions on the technical or security side.

Obviously you have a technical background but as a founder you also do sales. Is there anything that you like about sales?

I believe that as a founder of a startup you have to do a lot of different things and that includes sales. I have been an entrepreneur since I was 18. Since then I have been very active in technology and sales. It feels natural to me.

Moreover, it helps me to be in touch with our customers and know what our customers really want. So, it’s important for me to keep this contact with the end user.

How do you balance sales and tech?

That’s a tough one. Without tech there is no product, so you have nothing to sell but without sales you ultimately have no tech.

Therefore, it’s a balance that you have to find. During the initial years at Edda we were trying, learning, failing and repeating. Our main focus was almost exclusively on the product. However, things are much different today, we are now a profitable company and we’re in the development stage.

The team is growing and we have new challenges as well as new topics such as tracking performance of our marketing efforts, integration with third parties, enterprise deals and so on.

What are your most important challenges ?

As a B2B SaaS platform in Fintech, security is one of our biggest challenges. Indeed, we really need to be top notch on this particular topic. It requires us to be up to date about cyber security news and make sure that we are compliant with the latest security measures.

The platform is used everyday by VCs, Corporate VCs, LP’s, business angels and even banks. They are trusting us with their processes and data. Therefore, it’s our job to make sure that everything works properly and our platform is secured.

Another challenge is to hire great people for our team, I say people because it’s not just about being a good programmer or a designer, it’s not only about skills, it’s also about communication, independence and having the collaborative mindset.

What are your personal values that you would like to transfer to the entire company?

Freedom is very important to me. For instance, at Edda we’re encouraging everyone to be free to say what they think, as an intern or a CEO. Everyone has the power to influence the company. This is important for information to flow easily in the organization but also for everyone to feel good.

We’re almost a flat organization and I really believe this helps to avoid ego related issues and micro management.

Talking about management, do you have any mentors that inspire or guide you ?

I don’t really have one mentor, I try to analyze and learn from my surroundings to see what works and what doesn’t. I read a lot and this is where I find life lessons.

But, there is one person who has taught me a lot and it’s my father. He infused his business experience, tips, information and stories to become who I am today.

What is the most valuable lesson you learned as a CTO?

With the right team, you can create amazing things and thankfully at Edda, we have the best team.

Shakespeare said, “If you can look into the seeds of time, and say which grain will grow and which will not, speak then unto me”. In this quote, replace grain with startups and you get the basic thought that envelops the mind of VCs. In this post, I am going to talk about the importance of monitoring portfolio value as well as how to do it effectively.

After VCs make the first investment in a company, they are thinking about the additional capital requirement for future rounds and ultimately a successful exit. Therefore, having a dynamic portfolio monitoring system built into software venture capital tools can enhance the decision-making power of VCs.

1. Keeping track of valuation of your investments

Valuation of an investment is one of the significant indicators of how the company is performing. Subsequent changes in valuation signal where the company is heading. VCs continually ask portfolio companies to update their metrics. Using excel in such cases requires a lot of manual work (data entry and modelling) where VCs lose their valuable time. And this time can definitely be better spent on sourcing deals or managing the portfolio companies.

The Edda suite provides a platform where VCs can send an email to the representatives of the portfolio company (through the platform) to come to the platform and update the metrics. VCs can then monitor portfolio value of their investments in the portfolio value section, which gets updated with new information.

2. Forecasting the effect of future financing or exit

When you have all historical information in one place, easily accessible in a user-friendly way, the analysis becomes much easier. In order to make the right decisions, It is important to continually speculate future performance of portfolio company. This allows the VC to effectively plan for either additional capital in next rounds of financing to keep fueling the growth or not participate in the next round. In order to do speculation easily, it is essential to again have all information in one place and an option to quickly execute speculative scenarios.

One way to speculate in the Edda suite is to add data for probable future funding/exit directly from the Portfolio Value section. Then you can see how it changes the metrics (such as realized and unrealized IRR, proceeds) of the portfolio company. In fact, you can see the change in metrics for the entire portfolio. You can always delete such speculative funding decisions by clicking on the cross against the funding record from the funding table.

3. Performance comparison of portfolio companies

It is essential to compare the valuation of portfolio companies to see how different companies are evolving. Different portfolio companies operating in the same industry can show different valuations. For example, one is declining or stagnant while the other is growing. Such comparisons can assist the VCs in better allocating their time to manage the portfolio companies. Furthermore, it also empowers them to dig deeper and uncover new information about how successful/unsuccessful companies perform. As a result, they can use that knowledge to better manage new portfolio companies in the future.

The Portfolio Value section of Edda’s venture capital portfolio management software provides an easy to compare tool. Here with one click you can select the portfolio companies and compare their valuation over time. You can either compare companies separately or make groups of companies and compare them. You can always export all portfolio value data to Excel.

We are continually adding new features to our Edda suite to empower investors to better manage their investments. If you want to know more about measuring the performance of your VC fund click here.

Monday, besides being the least appreciated and most hectic day of the week, it is actually quite an exciting day for VCs. The VC Monday meetings are attended by the General Partners along with the investment team. The main purpose is for VCs to make decisions regarding new as well as existing companies in the dealflow.

The duration of the morning VC Monday meetings depends on the number of companies pitching to VCs. Usually, startups have to present a 40-45 slide deck under 45-50 minutes to VCs. Overall, the duration of Monday morning meetings can range from 3 hours to as long as 6.5 hours.

Admin Work – the mood killer

Now there is one character that acts like the adrenaline killer for VC Monday morning meetings. This character is none other than the Administrative Work. Namely, Analysts and Associates have to spend countless hours putting the data from the companies under consideration into powerpoint. This data consists of a brief introduction about the company, its business, industry and the associated metrics.

The pain doesn’t end here as they have to take notes about the minutes of the meeting for auditory purposes as well as make a note of the next tasks. Therefore, there is a lot of admin work which has to be done before, during and after the VC Monday meetings. There are numerous tools out there to make the life of VCs easier with regards to optimization of their internal business process. However, before making a decision, VCs should think about the level of integration, these tools can provide.

There is so much valuable time that can be spent elsewhere is wasted on the admin work. So, after addressing the boring elephant in the room, let’s talk about how you can redefine your Monday morning meetings. The dealflow section of Kushim Suite for VCs features an interactive and customizable dashboard that includes a special feature built in specifically to optimize Monday morning meetings.

Meet Dealflow Review

The dealflow review is a feature that eliminates the need to spend hours making powerpoint presentations while switching countless times between powerpoint and excel. All data about different companies in each stage of investment cycle along with the metrics is already present, so the dealflow review automatically takes all the data and creates a presentation. With just a click you can select the appropriate stages you want to review- watchlist, new, first meeting or due diligence and commence the presentation.

Real Time Response

Not only does the dealflow review simplify the admin work related to presentation, it also provides comment and task feature. You can make a decision whether to take the company to the next stage of investment or reject it during the presentation. As a result, the change will be reflected in your dealflow once you finish the review process.

What is more is the ability to assign the company to one of your team members and also assign a task which can be to ask the company for more metrics or data about new contracts they have procured. Additionally, you can also put in some comments for internal references using the “Add a comment” section.

Automatic Post Meeting Report Generation

When you click on the stop button to stop the review, you get the option to save the presentation. All saved meetings can be accessed from the “Committee” tab where you get two files saved per meeting. Both can be exported to PDF. The first report contains the slides of all companies that were reviewed along with their metrics and comments that were made during the review. The second one is the task list of your team members specifying which companies they are assigned to and their task.

Unlimited Storage

The dealflow review makes sure that you don’t have to waste your precious time. Neither for creating presentation nor for worrying about anything you might miss to jot down during the Monday meeting review. The unlimited storage ensures that you don’t have to worry about running out of space. All your Monday meeting reports are stored under the committee section which you can download any time.

If you want to know how you can build a better dealflow you can click here. Ready to start improving your dealflow now? Contact us and schedule your free trial of Edda’s venture capital software.

The objective of this article is to provide insights related to fundraising process for VC professionals. 2018 was a record year for the VC industry, in terms of investment $254 billion was invested globally. By the end of third quarter of 2018, VCs in US and Europe had raised more than $ 40 billion. The median fund size in 2018 was $83.7 million which is phenomenal as the median fund size in 2014 was $34.7 million. Keeping in mind the growing numbers of VCs fundraising, I am going to focus on three key considerations a general partner or an aspiring general partner should have in mind before raising the next or the first fund.

When Fundraising – Prioritize LP selection based on your decision criteria

Typically, the LPs of VC funds consist of pension funds, endowment and foundations, insurance companies, family offices, high net worth individuals, fund of funds and corporate funds. However, each LP has different risk profile and liquidity needs. For instance, insurance companies always have an uncertainty associated with their cash outflows. Hence they tend to invest a major portion of their money into risk-less assets such as bonds. In contrast, private foundations typically allocate more than 40% of their assets into alternative asset classes (i.e. PE and VC). Since their short term cash requirements are not high.

Elizabeth Yin, former Partner at 500 startups suggests that you must talk to a lot of fund managers to get advice about LPs rather than devoting your time and energy to approach institutional investors. While establishing her own VC fund, she focused on closing the fund as fast as possible and qualifying investors with smaller check sizes ($25K then going beyond $300K). The reason she prioritized on speed was because SEC in US mandates that you cannot market your fund while raising it.

Hence, relationship building and transparency are important factors while talking to LPs and especially institutional LPs. For new fund managers, closing an institutional LP can take more efforts and time. Therefore, they have to spend more time building relationships with institutional LPs.

Edda tip: Use a clear process to track the progress of your partnership with LPs. Here’s one of the best practices to setup a process:

New opportunities Initial allocation Legal/AML Final allocation Standby

Differentiate yourself by selecting a unique dealflow strategy or industry expertise

There is a gigantic gamut of VC funds out there. So, when fundraising, you have to think about what is the unique value proposition you can provide. Your UVP needs to separate you from the rest. Do you already have a network with ecosystem builders or a network with established founders to source startups? Does your team have a unique industry expertise that is going to help you find the next unicorns? These are some questions you must think about deeply before you start putting together your fundraising investment strategy.

The figure below illustrates the common categories of expertise of GPs.

Source: Concept adopted from The Business of Venture Capital 2nd Edition

Harvard professor Paul Gompers in his 2007 study on specialist vs generalist approach of VCs concluded that specialists performed better than generalists in VC firms that focused on a particular domain. On the other hand, if a specialist is put to manage a generalist role, the performance of the specialist weakens.

Thomas Meyer and Pierre Yves Mathonet, in their book, Beyond the J curve state the factors LPs consider on qualitative basis while conducting fund due diligence. Overall the management team’s skills, motivation and stability account for 50% of the qualitative factors LPs consider.

Edda tip: Get help from key industry players that can provide you with quality dealflow. In order to make this kind of partnership work, you need to standardize this process. At Edda we develop specific submission forms in our dealflow management software that populate your dealflow automatically.

Design an infallible investment strategy with your LPs

Chris Douvos, Managing Partner at Venture Investment Associates, who is also an LP, had interesting insights regarding GPs pitching. Namely, he states that oftentimes GPs make a pitch to LPs saying that they have designed a new investment strategy. However, they are unaware of the fact that ten or more such strategies have already been pitched to them. So how do you go about designing your investment strategy? Besides the competency and expertise of GPs there are some set factors that contribute to investment strategy.

Factors that contribute to investment strategy

The market size and growth opportunities– GPs must assess how big is the market they are going to target and the growth opportunities associated with it. Furthermore, what are the current trends and how will you be able to source the companies you want to invest in.

Capital requirement and investment returns- Key aspects to note here is whether you will have enough capital to meet the demands of your investment as well as have funds for follow on investment. Secondly, how long will the investment cycle be and most importantly will your approach actually aid you in getting the expected returns?

Risk Management- Just including a typical bunch of risks such as an act of God, currency risk, regulatory risk is not enough. As a GP you must think about the risks associated with your team and specific risks associated with your investment strategy. For example, if you are going with an investment strategy to invest in energy companies especially operating in emerging economies, then is there a regulatory or political risk that can prevent you from investing or that can tie your investment for a long time?

Edda tip: Involve your LPs in the investing process and share your dealflow with them. This is the most effective way to leverage their network, build transparency and engagement. Because we know how valuable this is for VC firms, we built a Portal into our deal flow management software where LPs can access dealflow companies. To make this process even more engaging, the LPs receive a monthly fully automated newsletter that redirects them to the Portal.

These are three broad factors that a GP must consider before raising a fund or going into the fundraising. In the upcoming articles, I will delve deeper into asset allocation strategies of different LPs. In addition, I will talk more about how different LPs conduct their fund due diligence.

After weeks or months of meeting, conducting due diligence, you have finally made an investment in a venture. However, now you can’t sit back and relax as the investment monitoring phase begins. One of the key success factors for a successful exit is to effectively monitor the progress of your portfolio companies. And choosing the right metrics for VCs monitoring is the key.

There are numerous metrics which can help you in monitoring process but it is essential to select the relevant ones. However, the relevant metrics for SaaS (Software-as-a-Service) companies won’t be the same as for the pharmaceutical company. Hence, our goal here is to depict which metrics are important for particular industries and how you can effectively track them with software venture capital tools.

VCs metrics for Marketplace Startups

For marketing place startups, one of the main metrics is the Gross Merchandise Value (GMV). It indicates the gross value of transacted goods and is calculated by the formula below:

GMV = Average value of an order x Number of transactions

However, one of the caveats associated with GMV is that it doesn’t take into consideration the value of discounts, returns, cancellations. Furthermore, it is not an indicator of revenue.

This can easily be seen in the chart example below which depicts the GMV of Alibaba from FY 2014-FY 2019 . In FY 2019 it was approximately CNY 5727 billion, while at the same time the revenue for entire Alibaba group stood at CNY 376.8 billion

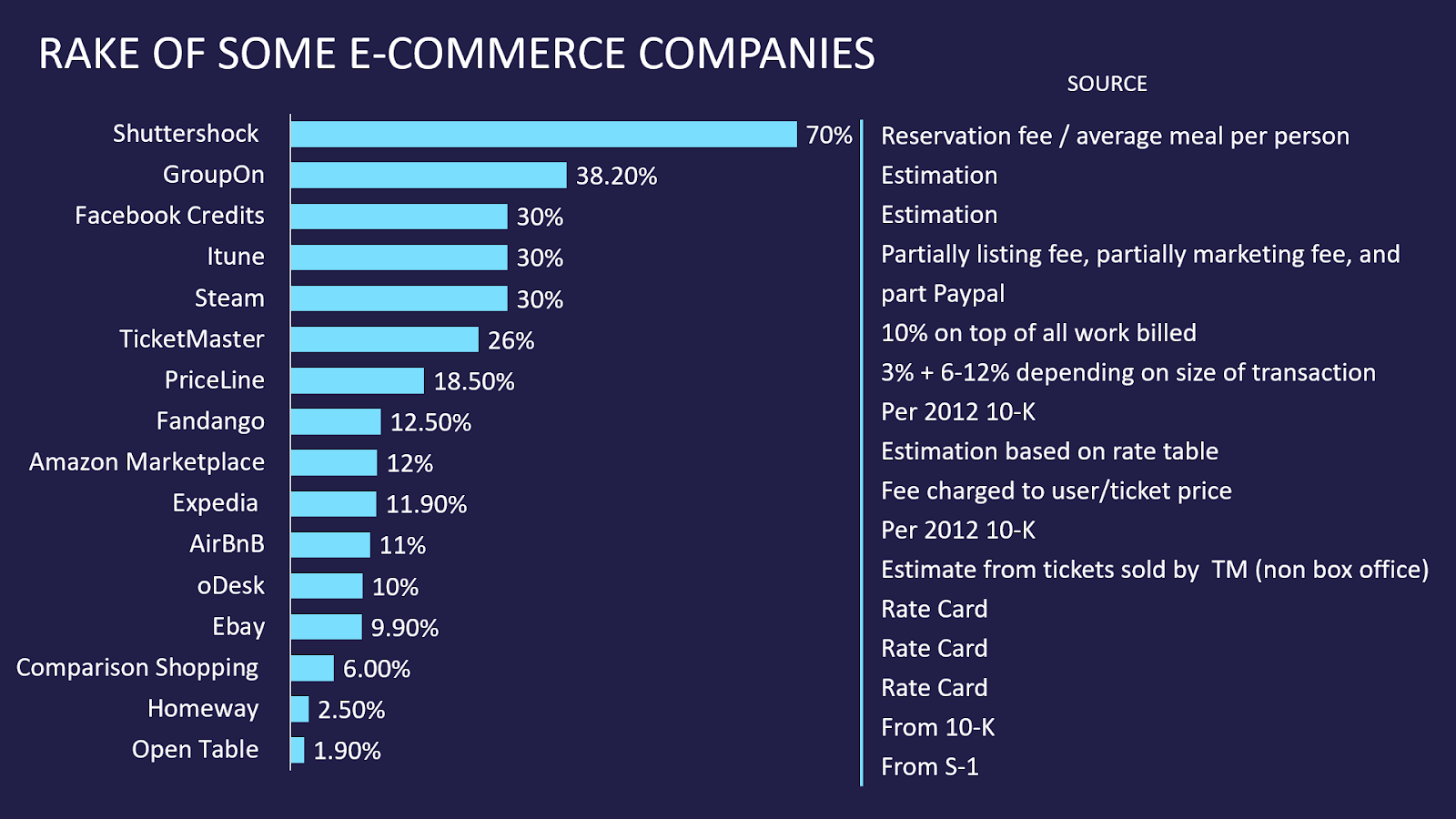

Take rate or Rake- refers to the percentage of sales and commission a company earns on its sales. For instance, Airbnb charges 3% from the hosts and a variable service fee from the guests which is somewhere around 11% but it decreases as the cost of booking goes up. Similarly this metric is important for payment processing companies as well.

The figure below shows the rake of some major e-commerce marketplaces:

SaaS Companies (B2B)

Product market fit

The first step to measuring performance of a B2B SaaS company is to assess the product market fit. This can be done by looking at the Annual Recurring Revenue or ARR and the cash burn rate. If a SaaS startup doesn’t have a product market fit then it will be burning more cash than its ARR. In such cases, the company is spending too much on acquiring new customers who are in turn leaving the product. As a result, the ARR is low. In a nutshell, the lack of product market fit is an indicator of unsustainable growth prospects.

ARR Calculation

In the most simple way, ARR = Monthly Recurring Revenue (MRR) x 12

However, the customer must sign up for a yearly subscription contract. Below I am mentioning some more cases to calculate ARR:

Growth prospects

After looking at product market fit, the next avenue to evaluate is the growth prospects. Typically for B2B SaaS companies, one of the growth benchmarks is T2D3 which translates to Triple, Triple, Double, Double, Double. This means that SaaS companies in Series A-B phase must show at least 3x growth year over year for three consecutive years and then show at least 2x growth.

The figure below shows T2D3 path of some prominent SaaS companies:

Source: Battery Ventures

Sales efficiency VCs metrics

One of the most popular VCs metrics for measuring sales efficiency of SaaS companies is the CAC (Customer-Acquisition-Cost) payback period. It shows the amount of time it takes a company to recover the cost it paid to acquire a customer.

VCs Metrics for SaaS Companies (B2C)

For SaaS B2C companies, the top metrics to look at are: Customer Chrun Rate, Revenue Chrun Rate, Customer Lifetime Value and Leads to Customer rate.

To start with, the Customer Churn Rate measures the number of customers a company has lost over a specified period of time.

Furthermore it is very important to calculate the Revenue Churn Rate because different customers can have different revenue weight-age. For example, losing five customers who pay $5000/year is less disastrous than losing a single customer that pays $45,000/year.

In addition, the Customer Lifetime Value denotes the average amount of money a customer pays during the whole engagement period with your company. It is calculated by finding the customer lifetime rate followed by average revenue per account.

Finally, the Leads to Customer Rate depicts the percentage of leads that were converted to customers.

VCs Metrics for Pharmaceutical Startups

As aforementioned, different industries will require different metrics for performance assessment. Hence, here we will discuss the relevant VCs Metrics for the pharmaceutical industry.

In order to show a strong standing the company must have a large number of discovered molecules and a significant number undergoing clinical trials.

Furthermore, an extremely important metrics is the R&D Spending. This metric is calculated by looking at the total amount of funds spent on R&D initiatives and comparing it to the amount spent on completing the development of products in the end cycle. Therefore, a small R&D spending is an indicator of lack of innovation and reluctance to adopt new technology.

In addition, Investment to IP ratio will depict how successfully the company is utilizing its R&D efforts to get more Intellectual Property (IP). The higher the number of IPs the better.

Moreover, the number of partnerships with other pharma companies is yet another sign of growth and credibility.

Finally, the Team Structure, or the number of specialists in each section is a very important indicator. Typically the team should have the following structure: 33% biochemistry specialists, 33% AI specialists, 33% investor relations and business development. As a best practice, the number of biochemistry specialists should not be less than 10.

How to track all these metrics?

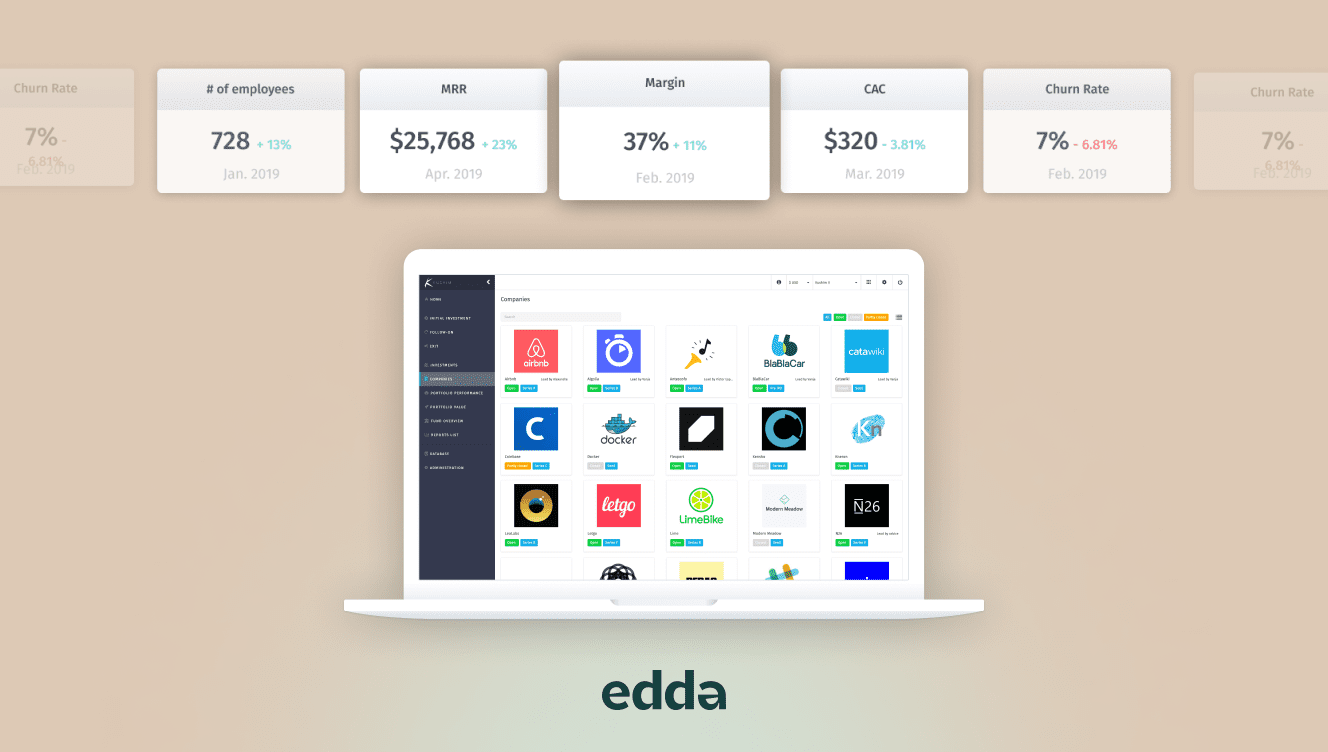

Evidently, there are countless metrics for tracking the performance of the portfolio companies. However, the burning question here is, how do you keep track of all the relevant metrics? And the answer is the Edda Management Suite which fetches you the most user friendly solution.

Clean, Precise and User Friendly

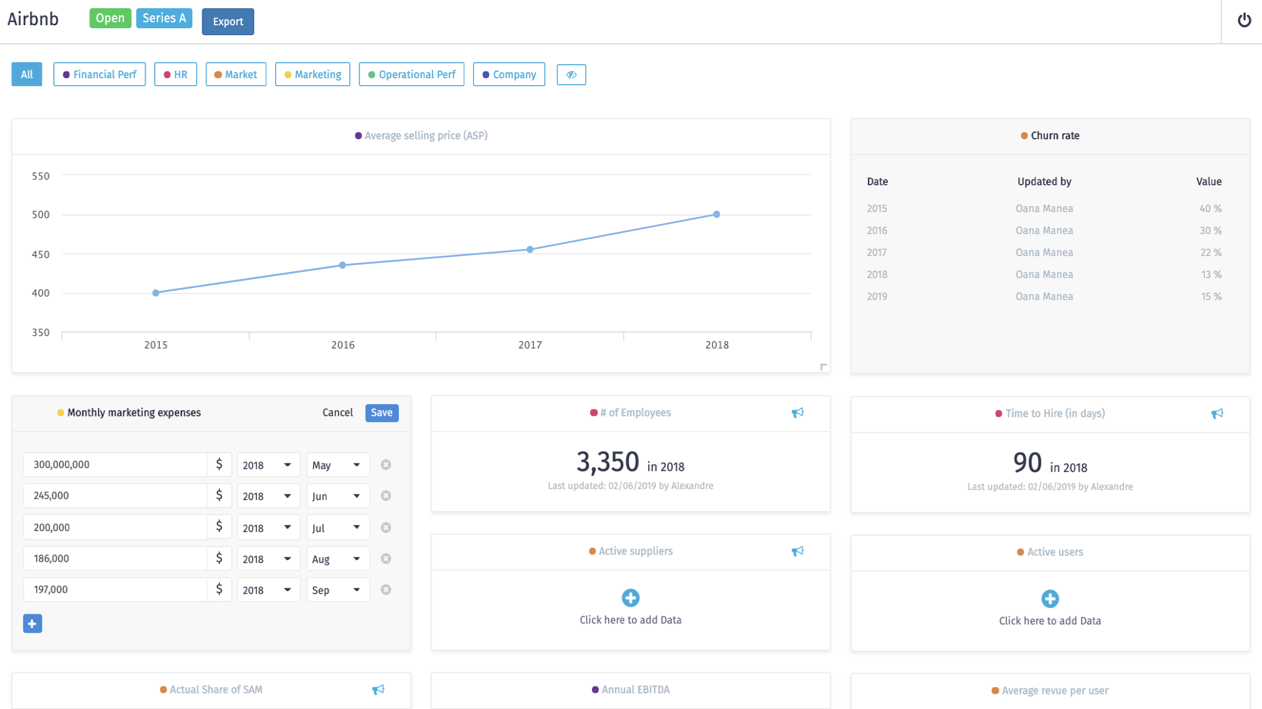

The “Companies” section of Edda’s Management Suite illustrates all companies in your portfolio in a precise and user friendly way. It also provides a quick search option.

One size CAN fit all

With a click you can open the company page which contains its details along with the section for captable and metrics. By default you have 60 different metrics which are well organized and categorized. Some of the categories include: Financial performance, HR, Market, Marketing, Operational Performance and Company.

You can select the metrics which are relevant to you and also create new metrics.

Stay Updated

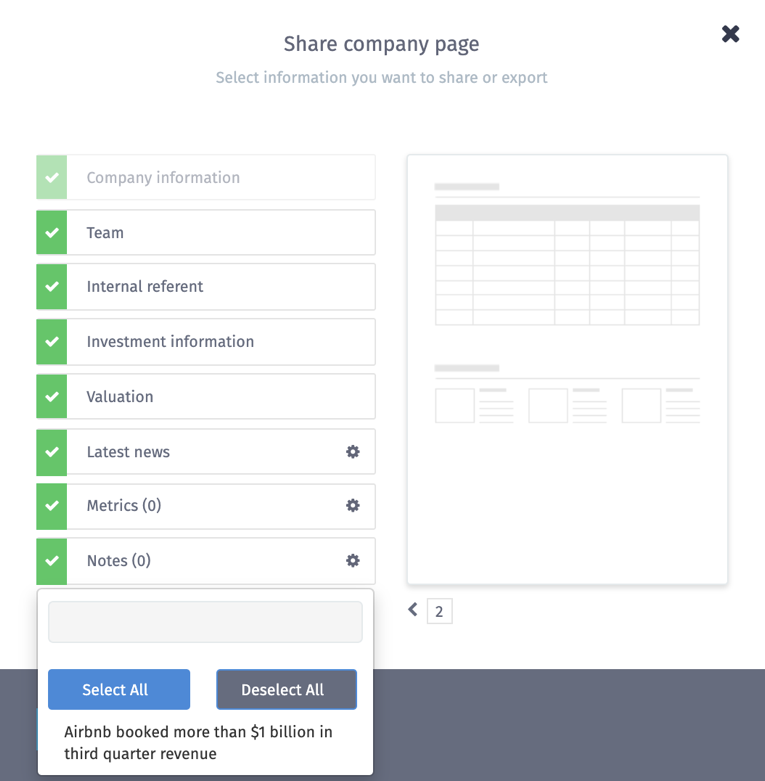

With venture capital management software you can grant access to your portfolio company’s page for the officials of that particular company. In addition, with one click you can send an email to the company representatives to ask them to metrics updates. You can also export company details including the metrics to PDF using the Export button.

Finally, besides the metrics, the Edda Management Suite can do a lot more of the heavy lifting for you. Want to know how it can help you measure the performance of your entire fund or funds?

That’s all for this post! If you are interested, we have compiled a list of 200+ metrics for SaaS, Pharmaceutical, Social Impact, Real Estate and many more industries.

When we say VC fund performance, the first metric that comes up is the Internal Rate of Return or IRR. Indeed, investors typically compare the fund performance with the aggregate returns generated by an entire VC asset class. For instance, let’s say that a specific fund of a certain vintage year generated 34.5% IRR then an investor would use this to compare with appropriate benchmarks.

However, in this process, there are some caveats-

The Vintage Year Temptation Sometimes fund managers are tempted to assign vintage year when he started raising the fund not when the final close happened.

The Categorisation Issue There is a gigantic gamut of universes to compare. Of course, it is a good practice to position your fund in an appropriate category to avoid comparing apples with oranges. For instance, the appropriate categories can be: a) All Early stage VC funds or Technology VC funds or b) All French early stage technology VC funds

The Peril of Unrealized Returns It is a good practice to not include unrealized returns in calculating fund performance as unrealized returns are risky since value of shares held in a private company can often exhibit large deviation.

The Precision of data In general, VC industry has the self-reporting culture and often LPs have opinionated that mostly the mediocre managers report data.

DRAWBACKS OF IRR

According to an informal research done by McKinsey in 2004, only 20% of executives understood the critical drawbacks of IRR. For instance, if you compare two funds, one with an IRR of 24% with that of 11%, one would be inclined to regard the first fund as better performing. However, the devil here is again in the details. This is due to the fact that the IRR is not telling us the reinvestment risks and capital redeployment in other investment opportunities.

Next, the IRR is a percentage and so there is a case where a small investment can show a big double digit or a triple digit IRR while a large investment can show an IRR of single digit but be more lucrative once it is accounted for the net present value (NPV).

OTHER VC FUND PERFORMANCE METRICS

Besides IRR, some LPs are also using metrics such as COC, TVPI or DPI to measure the performance of a VC fund. using metrics such as.

Cash-On-Cash return (COC) In VC and PE landscape, COC multiple shows how much return the fund received after exiting the investments. Of course, the investors will always prefer an investment with 40% IRR over a 5 year period with 4x COC over an investment with 100% IRR over a 1 year period with 2x COC. The COC multiple of an entire fund helps the LPs know how much carried interest will be available to split.

To explain the next multiples, we will first introduce some terminology which is used to calculate the multiples listed below:

Paid in Capital This refers to the capital contributed by the LPs to a fund. It is also known as “Contributed Capital”.

Distribution This is the value of cash stocks that is given back or distributed by the fund to the LPs.

Residual Value It is the remaining value of a fund at a given point in time. It is calculated by adding fair value of all remaining investments plus any cash equivalents minus any liabilities.

Total Value (TV) The total value of a fund is the sum of Residual Value and Distribution.

TV = Distribution + Residual Value

The figure below shows an illustration of the terminology discussed above.

Now let’s have a look at different multiples

Distributions to Paid-in Capital (DPI) It is calculated by dividing distributions by paid-in capital.

A DPI of 5x means the fund provided a return to LPs that was 5 times the paid-in capital. Therefore, LPs desire a higher DPI multiple.

Residual Value to Paid-in Capital (RVPI) It is calculated by dividing residual value by paid-in capital.

Total Value Paid-in Capital (TVPI) It is calculated by dividing the Total Value by Paid-in Capital.

Since Total Value = Distribution + Residual Value

Hence, TVPI = DPI + RVPI

ENTER THE PUBLIC MARKET EQUIVALENT (PME)

Besides IRR, the other multiples discussed above serve as a good metric to measure the performance of a fund. However, there is another measure called Public Market Equivalent which basically measures the performance of a fund compared to a public market index such as S&P 500. A fund having a PME of more than 1 indicates that the LPs received better return by investing in the fund rather than investing in the market.

Let’s say an LP invested $100 million in a fund and received $500 million after 5 years. In the same time frame, had the investor invested in S&P 500, he would have earned $395 million. So the gross PME = 500/395 = 1.26. In this case, the investor didn’t lose money by investing in VC fund as the PME is greater than one.

What I have described above is a simple way to calculate PME, there are different forms of PME which have been developed over the years such as LN PME, KS PME, mPME, PME+ and Direct Alpha.

The fund performance section offers all the information about your fund’s performance and all the multiples mentioned above are calculated as well.

You want metrics? Here they are!

Kushim’s venture capital management software offers 60 in built metrics to measure the performance of your portfolio companies. In addition, keeping in mind the bespoke nature of our solutions, now you can add your custom metrics. Moreover, you can even send an email directly from Kushim Management suite to your portfolio company and invite them to update the metrics.

The representative of your portfolio company will only be able to access the company page of his/her company and update the metrics.

Reporting simplified

The software venture capital tool offers dynamic data about your portfolio’s performance that can be exported to Excel with a single click.

The report generation tool

For those who love analytics and want to create custom reports, the Kushim venture capital software features a report generation tool that is dynamic in nature. All you need to do is select the type of data you want to compare and create dynamic reports that can be downloaded any time.

These are some of the salient features of Kushim’s venture capital software. If you would like to know more click on the below button to book a demo.

Finally, in this article we have presented some of the basic metrics for measuring the performance of a VC. If you would like to read more on advanced methods for measuring a fund’s performance click here.

Source:

John C. Kelleher and Justin J. MacCormack, “Internal Rate of Return: A Cautionary Tale,” McKinsey Quarterly, October 20, 2004.

The Business of Venture Capital by Mahendra Ramsinghani