At some point, we have all heard about the saying: “Networking is the key to success”. In this article, we will talk about Venture Capital firm networks for and their benefits.

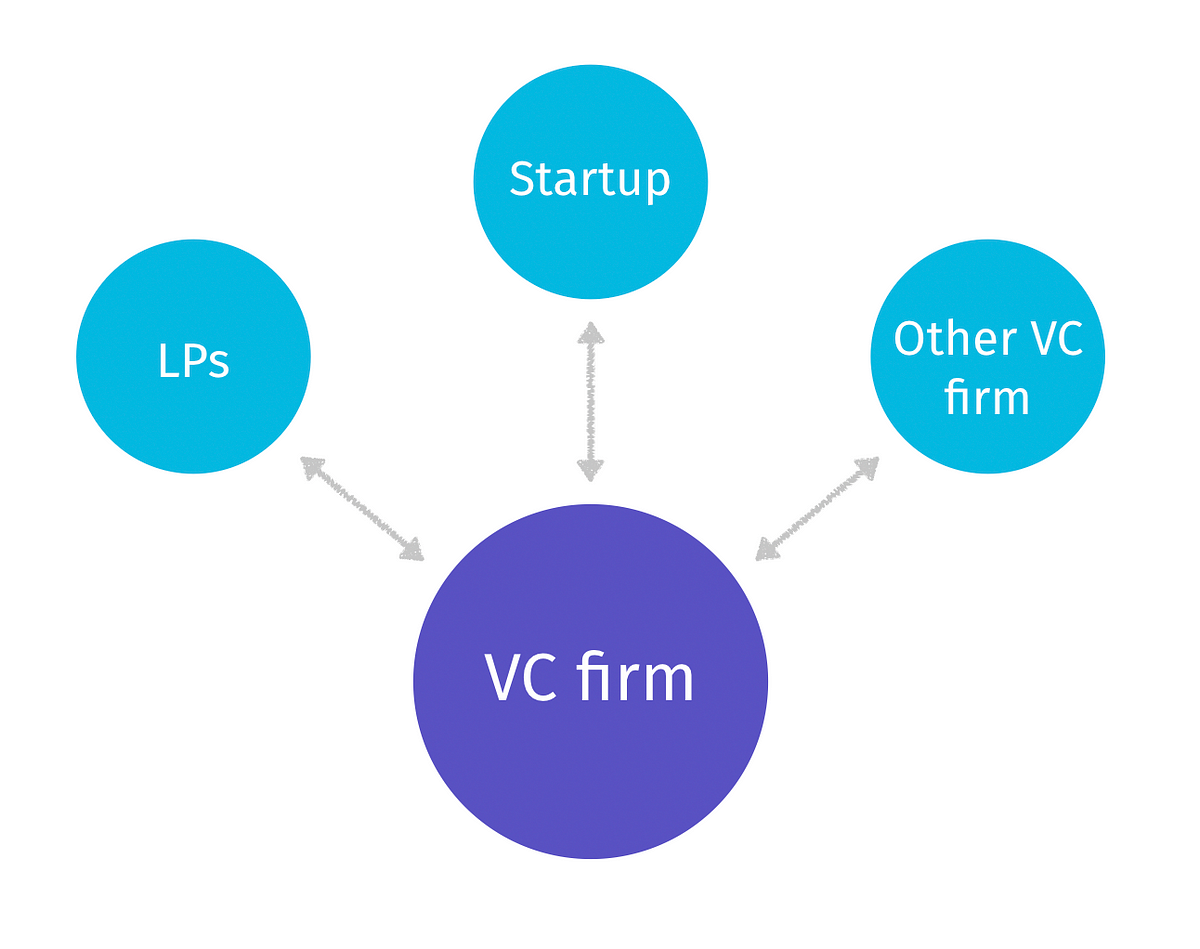

The VC landscape is full of networks, however the best and most common example of a VC firm network is syndication. Syndication refers to a situation where two or more venture capital firms join forces to make the complete investment for a particular round. In this arrangement, one of them is taking the role of the leader.

In many cases, syndication occurs even when a the funding requirements are modest. This is exactly one of the questions we will address here through providing some empirical evidence. We will talk about the findings of one study which focuses on the Canadian VC industry. In addition we will also discuss another study which focuses on the UK and European VC market.

The Canadian study was conducted by researchers from the University of Pennsylvania and University of British Columbia. While the European study was conducted by researchers from the London School of Economics and University of South Hampton.

The Canadian Study

The Canadian study set forth to test two theories associated with networking effect. The first theory is the selection theory which basically means that VCs want a second opinion from other VCs before making a decision. The second theory is the value-addition theory which means that VCs go for syndication because it is more beneficial.

Empirically, if syndication is done for selection then the exit return on syndicated investments should be lower than standalone investments. Alternatively, if syndication is done for value-addition then syndicated investments should have higher exit return than standalone investments. The sample size consisted of divestitures of VCs from 1992 till first quarter of 1998.

The total observation set consisted of 584 exits but only 393 were considered as annualized returns couldn’t be calculated for the remaining 171 exits. The study defined syndication as “narrow” and “broad”. A narrow syndication was defined as a situation where, let’s say investor A invests and exits and investor B invests. All this happens in a year. In broad syndication the time period is taken as 6 years. Of the 393 exits there were 147 narrow syndications and 194 broad syndications.

After talking too much about the data, let’s look at the results. The findings indicated that syndicated investments had on average higher return than standalone investments. This finding affirmed the value-addition theory i.e. VCs seek syndication to add more value to their portfolio companies. However, the study also stated that the selection-theory effect is not completely absent. So, there are some instances where VCs seek syndication for second opinion.

The European Study

Now let’s move on to a more recent study involving VCs in United Kingdom and Continental Europe. In the Canadian study we saw that syndication offers better returns than standalone investments. The European study goes deeper to see what happens when syndications are coupled with more relationship-building efforts. The study consisted of 624 VCs and examination period was 1995-2005.

Firstly, the study investigated the effect of GP’s networking with other investors while they sit on the board of portfolio companies, on the fund’s performance. This benchmark analysis yielded that GP’s with more experience and stronger network improves a fund’s performance.

Secondly and lastly, the study wanted to test the extent to which networking benefits fund performance. The results suggested that VC firms get large benefits when they have many ties. These benefits increase when a VC is invited to join many syndicates or when they are well connected to other VCs.

But when VCs act like an intermediary i.e. an agent between two other VCs, there is no significant added value on the fund’s performance.

So, in a nutshell, networking is beneficial for VCs when they are taking part in different investments.

Want to know more about how Kushim facilitates networking among VCs?

Click here to meet our software venture capital portal.