In venture capital, particularly in the arena of seed-stage investments, the ability to effectively scale deal flow management is a critical challenge. As these firms expand, they often face the limitations of commonly relied-on, yet basic tools like Airtable, which can lead to operational inefficiencies and the risk of missing significant investment opportunities.

This article explores advanced portfolio management tools that are specifically designed to meet the growing needs of venture capital firms. These tools extend beyond basic functionality, offering enhanced integration and management features essential for effective and agile operations in the expanding venture capital sector.

Understanding the Needs of High-Volume Deal Flow Management

As venture capital firms grow, they encounter an escalating scale and complexity in their deal flows. This increase is not merely numerical but also involves a diversification of investment types, sectors, and geographies. For instance, a firm that once managed a dozen local investments may now juggle hundreds of deals spanning multiple regions and industries.

Each of these deals comes with its own set of variables – differing business models, market dynamics, regulatory environments, and growth trajectories. This diversity necessitates a nuanced approach to evaluation and management.

Consequently, venture capital firms require tools that can not only handle a higher quantity of deals but also offer the flexibility and sophistication to manage this complexity. Relying on basic tools can lead to a bottleneck, where the sheer volume and variety of data overwhelm the firm’s capacity to process and respond effectively.

Integration with Existing Systems

The challenge of scale and complexity is further compounded by the need for integration with existing systems. A typical venture capital firm uses many tools for different purposes – from communication platforms like email and messaging apps to data analysis and reporting software. As the dealflow increases, the interplay between these systems becomes more critical.

Effective integration capabilities allow for a seamless flow of information across these platforms. For instance, when a new deal is entered into a deal flow management system, relevant data should automatically be accessible in the firm’s communication tools, analytical software, and reporting systems. This level of integration ensures that critical information is readily available, reducing the time spent on manual data entry and cross-referencing.

Moreover, well-integrated deal flow management software enables a more cohesive and holistic view of each potential investment. This is crucial in a high-volume environment where the risk of missing key details is high. Integration also supports better collaboration among team members, as everyone has access to the same, up-to-date information, irrespective of their specific roles or the tools they primarily use.

Limitations of Airtable in High-Volume VC Environments

The volume and complexity of deal flow can be overwhelming for Airtable. The platform, while suitable for moderate data management, struggles with extensive, multifaceted investment data.

Its performance often lags when handling large datasets, and it lacks the advanced analytical features necessary for complex deal evaluations. This limitation necessitates additional tools or manual processes, hindering efficiency.

Integration is another critical area where Airtable falls short for VC firms. Effective workflow in VC requires seamless integration with a range of tools, including deal flow CRM systems, financial analysis software, and communication platforms.

Airtable’s integration capabilities are limited, leading to fragmented workflows and manual data transfers. This disconnect results in inefficiencies and a higher risk of errors, as real-time data synchronization across various platforms is not fully supported.

Exploring Alternatives to Airtable for VC Firms

In the quest for more efficient deal flow management, venture capital firms must look beyond generalist tools like Airtable. Two categories of alternatives stand out: advanced Customer Relationship Management (CRM) systems and specialized deal flow management tools, each offering unique benefits tailored to the specific needs of VC firms.

Advanced CRM Systems

Advanced CRM systems have evolved far beyond mere contact management. For VC firms, these CRMs can act as powerful hubs for managing investor relations, tracking potential investments, and maintaining extensive databases of startup information.

- Customization for VC Needs: Modern CRMs offer customizable modules that can be tailored to the specific workflows of VC firms. This includes managing communications, tracking investment rounds, and monitoring portfolio company performance.

- Data Analysis and Reporting: Advanced CRM systems provide robust CRM data entry and analysis tools. They can aggregate data from various sources, offering insights into market trends, investment opportunities, and portfolio performance. This feature is particularly valuable in making data-driven investment decisions.

- Integration Capabilities: A significant advantage of these CRMs is their ability to integrate with other tools used by VC firms, such as financial modeling software, email platforms, and internal communication tools. This facilitates easier CRM user adoption and ensures efficient workflow.

Specialized Deal Flow Management Tools

Specialized dealflow management software is designed with the unique needs of VC firms in mind. These tools focus specifically on streamlining the process of managing a high volume of investment opportunities.

- Deal Sourcing and Tracking: These tools excel in organizing and tracking the numerous stages of deal sourcing, evaluation, and closure. They provide a systematic approach to managing the deal pipeline, ensuring that no potential investment slips through the cracks.

- Collaboration Features: Given the collaborative nature of venture capital decision-making, these tools often include features that facilitate teamwork, such as shared notes, evaluation forms, and communication threads tied to specific deals.

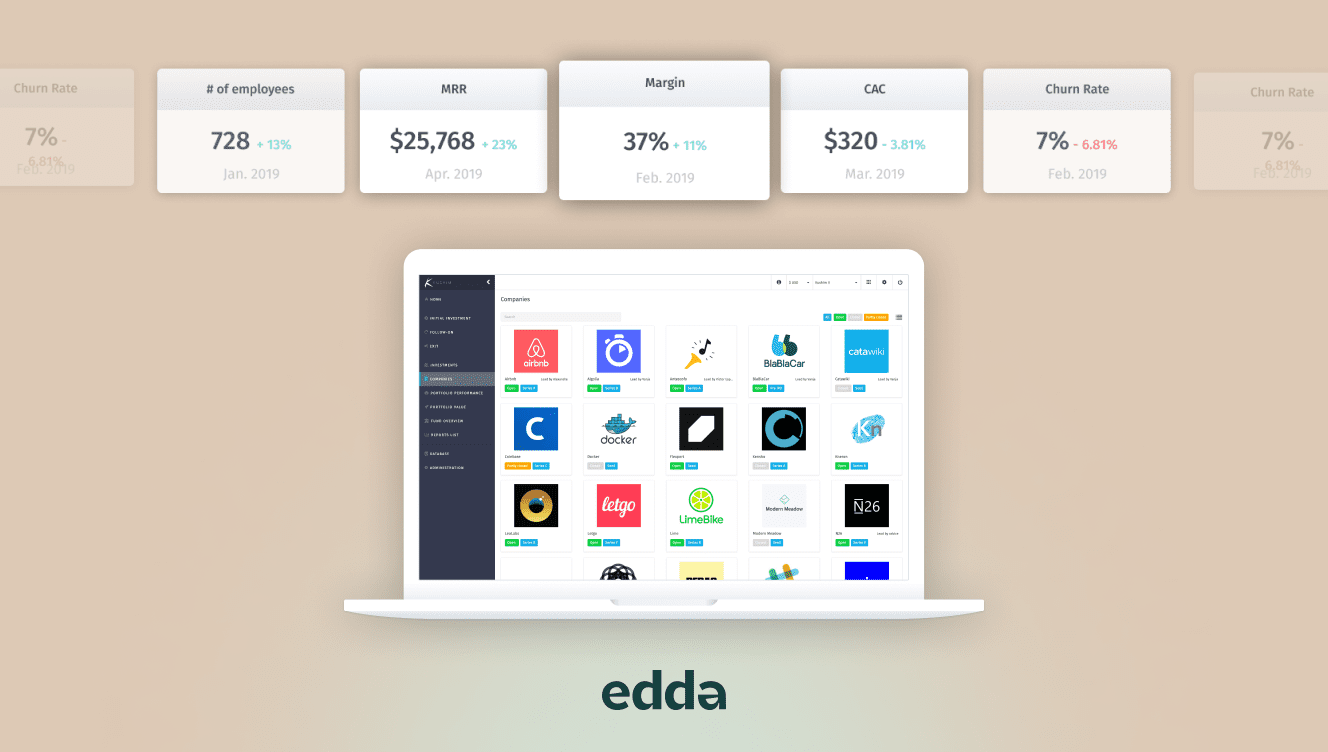

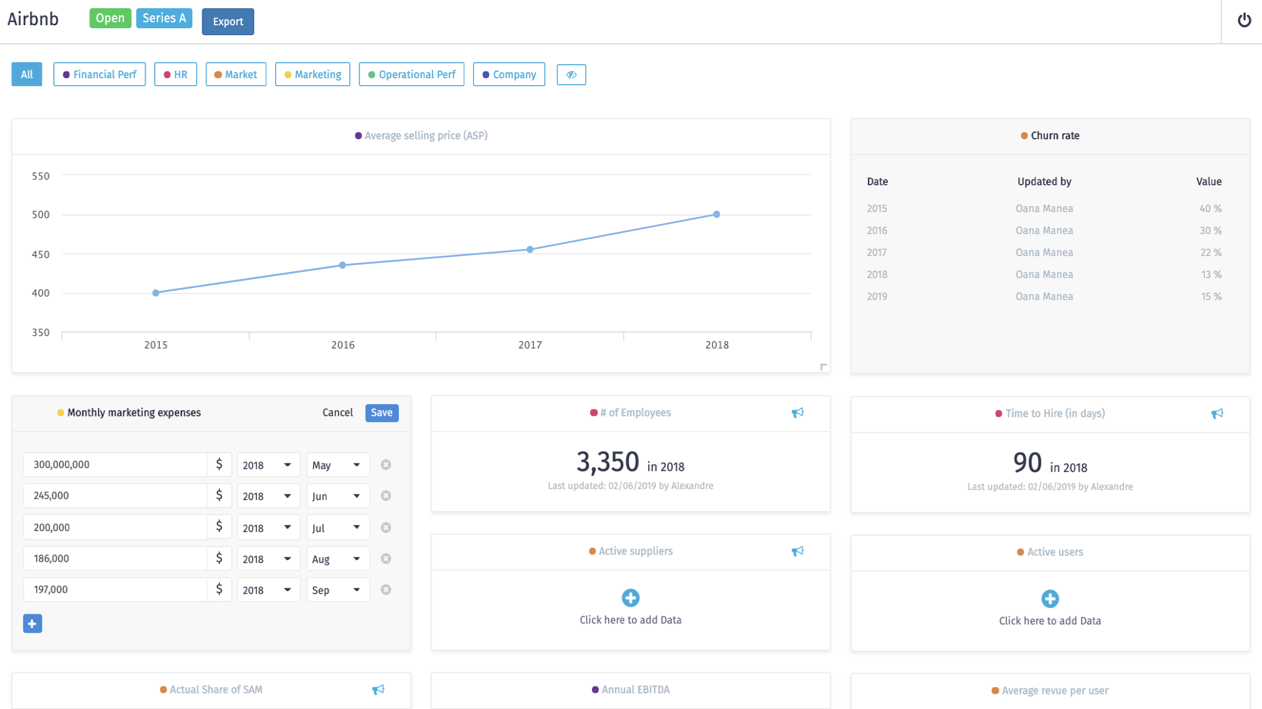

- Portfolio Monitoring: Besides managing prospective deals, these tools often include features for monitoring the health and progress of current investments. They provide dashboards that display key metrics and milestones for portfolio companies.

While Airtable has its merits, VC firms dealing with a high volume of complex deals require more specialized solutions.

Advanced venture capital CRM systems offer a comprehensive approach to managing relationships and data, while specialized deal flow management tools provide targeted functionality for managing and tracking investment opportunities. Both types of tools bring a level of sophistication and integration that is crucial for the efficient operation of growing venture capital firms.

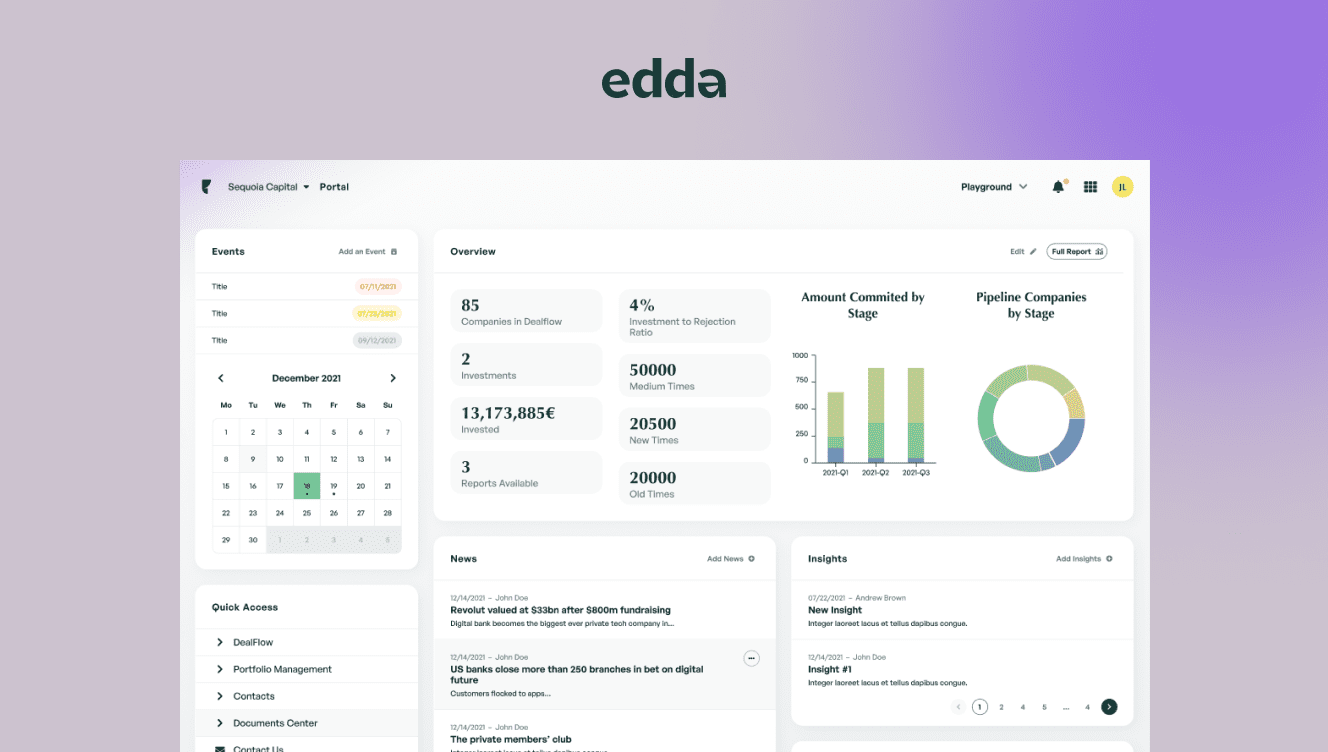

Scalability, Integration, and Usability: The Edda Advantage

Edda stands out as a comprehensive deal flow CRM solution for venture capital firms, adeptly addressing the critical needs of scalability, seamless integration, and user-friendliness.

Scalability and Flexibility

Edda is designed to grow with VC firms, adeptly handling the expanding scope of deal flows and portfolio management. Its proven capability to manage over $30 billion in assets across numerous countries underscores its robust scalability and flexibility, catering to the evolving demands of both emerging and established VC firms.

Seamless Integration

Integration is a key strength of Edda. It seamlessly connects with vital platforms like email clients and data analysis tools, enhancing efficiency. The integration with PitchBook, for instance, exemplifies how Edda streamlines data flow and analysis, crucial for informed decision-making in VC operations. The added mobile app access ensures continuous workflow across various devices.

User-Friendly Interface

Edda’s interface is intuitively designed, making it accessible for all team members, regardless of their technical expertise. This user-centric approach facilitates effective team collaboration and ensures that the platform’s comprehensive features, from CRM to portfolio management, are fully leveraged for optimal operational efficiency.

Edda’s scalability, seamless integration with essential tools, and intuitive interface make it an exemplary choice for VC firms seeking an efficient and adaptable dealflow management software.